XiamenApril 30, 2026 /PRNewswire/ — The following report is from the Strait Herald:

Turning Point in Performance Established: From Scale Expansion to Quality-Driven Growth

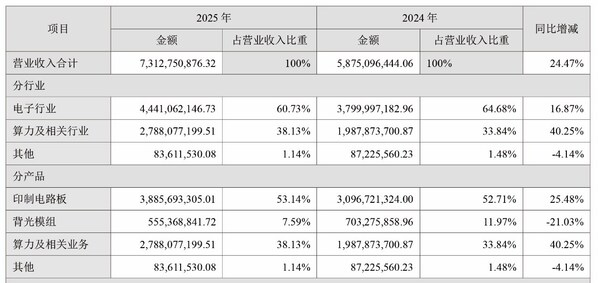

Financial report data shows that the company achieved operating revenue of 7.313 billion yuan in 2025, a year-on-year increase of 24.47%; net profit attributable to the parent company reached 147 million yuan, a year-on-year increase of 159.13%. Achieving high profit growth while fully provisioning for impairments and digesting historical burdens reflects a simultaneous improvement in the company’s earnings quality and asset structure.

This trend was further reinforced in the first quarter of 2026. During the reporting period, the company achieved operating revenue of 1.617 billion yuan, a year-on-year increase of 1.85%; net profit attributable to the parent company reached 37.9188 million yuan, a substantial year-on-year increase of 457.57%. Against the backdrop of the traditional off-season in the electronics industry, profit growth significantly outpaced revenue growth, indicating a combined effect of operating leverage release and business structure optimization.

Meanwhile, the company’s contract liabilities increased by 308.4% year-on-year to 164 million yuan, primarily driven by growth in advance receipts from computing power business, indirectly confirming sustained high demand downstream. Overall, the company’s growth paradigm has shifted from “scale expansion-driven” to “quality and efficiency-driven.” Profit growth is increasingly fueled by technological capabilities and product structure upgrades, reflecting the endogenous logic of enhanced product value and improved gross margins. The turning point in performance has been officially established.

Core FPC Business: Completing the Cyclical Reversal, Technology Upgrades Drive Profit Center Upward

As the traditional core business, the Flexible Printed Circuit (FPC) segment has achieved a critical leap from losses to profitability after navigating industry cyclical fluctuations.

In 2025, the company’s FPC business achieved main operating revenue of 3.886 billion yuan, a year-on-year increase of 25.48%; the gross margin improved to 9.97%, an increase of 7.22 percentage points year-on-year, indicating a significant improvement in operational quality. In the first quarter of 2026, during the industry off-season, the FPC business still achieved revenue of 785 million yuan, a year-on-year increase of 7.01%, and net profit increased by 126.76% year-on-year, demonstrating profit stability with a “non-off-season” characteristic. The driving factors include the company’s proactive optimization of order structure, increasing the proportion of high-value-added products, and improving costs through supply chain integration and production efficiency enhancements.

More critically, the company’s forward-looking布局 in high-frequency, high-speed materials such as LCP and MPI positions it favorably in the trend of AI terminal hardware upgrades. With the expansion of application scenarios such as AI terminals, servers, and wearable devices, the FPC business is evolving from traditional consumer electronics support to “high-performance connection and transmission solutions,” with its manufacturing attributes continuously transitioning towards technology attributes.

Computing Power Business: Accelerating Service-Oriented Transformation, Continuously Optimizing Profit Structure

Compared to the recovery of the FPC business, the computing power business has become the core engine driving the company’s growth. In 2025, the company’s computing power and related businesses achieved operating revenue of 2.788 billion yuan, a year-on-year increase of 40.25%, with its share of total revenue rising to 38.13%.

Among these, comprehensive computing power resource services performed particularly strongly, achieving full-year revenue of 578 million yuan, a substantial year-on-year increase of 229.62%, and its share of computing power business revenue rose to 20.72%. This structural change marks substantial progress in the company’s transformation from hardware sales to a high-margin service model.

In the first quarter of 2026, this trend continued, with the computing power business achieving revenue of 726 million yuan, of which comprehensive computing power resource services revenue was 171 million yuan, a year-on-year increase of 25.46%, and the gross margin improved to 34.46%. The increase in the proportion of high-margin businesses directly drives the improvement of overall profitability and also reflects the transformation of the company’s revenue structure from hardware sales to technical services and platform capabilities, with continuously enhanced technology attributes.

In terms of business model, the company adopts a “comprehensive computing power resource services + equipment sales” model and introduces a “Token sales” service mechanism, converting one-time equipment revenue into recurring service revenue, enhancing business sustainability and profit stability.

From an industry perspective, with the continuous implementation of large models, autonomous driving, and AIGC applications, computing power demand is entering a phase of rapid release. By securing computing power resources in advance and deploying computing power infrastructure, the company is poised to benefit continuously from the industry’s high prosperity cycle.

Technology and Ecosystem: Full-Chain Capabilities Support Strategic Leap

Behind the business structure upgrade is the company’s continuous increase in technology investment and ecosystem construction. In 2025, the company’s R&D investment reached 140 million yuan, a year-on-year increase of 13.69%, focusing on two main directions: “physical layer connection capabilities” and “digital layer computing power capabilities,” gradually building a full-chain technology system.

In the FPC field, the company focuses on high-frequency, high-speed transmission needs for AI terminals, promoting the upgrade of material systems to LCP and MPI, and accumulating expertise in key processes such as low-profile copper foil and precision impedance control, strengthening mid-to-high-end application capabilities.

In the computing power field, the company has formed a “hardware-system-platform-service” technology architecture: at the hardware and system layer, it launched the “Suhong Domestic Super Node,” enabling clustered delivery and high-density deployment of computing power; at the platform layer, it built the “Suhong Intelligent Computing Cloud Platform,” achieving unified management and scheduling of heterogeneous computing power; at the application layer, it created the HonMaaS platform, promoting the transformation of computing power into model services, enhancing computing power utilization efficiency and value output capabilities.

At the same time, the company continuously improves key supporting capabilities, forming technical support in areas such as liquid cooling system integration, server architecture optimization, and computing power scheduling, strengthening comprehensive solution capabilities for high-density computing power scenarios.

In terms of ecosystem construction, the company collaborates with leading enterprises such as Huawei and Lenovo, achieving technological complementarity in computing power infrastructure and platform capabilities; it partners with universities like Tsinghua University and Shanghai Jiao Tong University to advance cutting-edge technology research and development; and it continuously collaborates and innovates with the upstream industry chain in key areas such as chips, optical modules, and liquid cooling.

Overall, the company has achieved an evolution from manufacturing capabilities to full-stack computing power capabilities, laying the foundation for its long-term competitiveness in the AI computing power industry and marking its accelerated transformation towards a technology-driven technology enterprise.

Financial Structure Optimization: Improved Cash Flow Supports Medium-to-Long-Term Expansion

During the business expansion process, the company’s financial structure has simultaneously improved.

In 2025, the company’s cash and cash equivalents balance at year-end increased by 396 million yuan. In the first quarter of 2026, the company’s cash reserves significantly increased, and operating cash flow improved by over 70% year-on-year, indicating continuously enhanced cash generation capabilities of the main business; the current ratio improved, further enhancing short-term debt repayment capacity.

In terms of financing strategy, the company has gradually shifted from “scale-oriented” to “efficiency-oriented,” optimizing the financing structure and controlling capital costs, providing support for subsequent computing power infrastructure construction and business expansion.

On this basis, the company fully embraces a “light asset” operating model, leveraging the “Cloud Innovation Computing Valley” ecosystem to promote regional replication of the computing power business, and improving resource utilization efficiency and service reuse capabilities through the MaaS platform.

At the same time, the company is advancing the construction of a GW-level AIDC computing power factory centered in Qingyang (with a total investment of approximately 12.8 billion yuan). Against the backdrop of heavy asset investment, the company achieves a balance between expansion capability and financial stability by optimizing the financing structure and investment pace, providing support for medium-to-long-term development. Driven by technology upgrades and business structure optimization, the company’s overall gross margin and operational quality show a continuous improvement trend.

AIDC Computing Power Factory Planning Diagram

Against the backdrop of accelerating evolution in the artificial intelligence industry, computing power infrastructure is transitioning from a “supporting element” to a “core productive force,” and industry competition has upgraded from single equipment capabilities to a comprehensive competition of “resource acquisition + system integration + platform operation.” In this trend, enterprises with synergistic capabilities in manufacturing foundation and computing power services hold greater strategic value. Hongxin Electronics, leveraging FPC to enter the physical layer of AI hardware and extending to computing power equipment, cluster systems, and service platforms, is gradually forming a dual capability structure of “smart manufacturing + computing power services,” with its growth logic shifting from cyclical recovery to structural growth.

Overall, the company has crossed the performance turning point. Driven by the dual engines of “flexible electronics + inclusive computing power,” it is evolving from a manufacturing enterprise to an intelligent infrastructure service provider. As AI computing power demand continues to be released, driven by improvements in technological capabilities, increases in product added value, and continuous optimization of the business structure, the company’s long-term growth space and value logic are gradually entering a phase of realization.